Expert says Ky. is one of 13 states where people in individual insurance market are better off than before reform law

Kentucky Health News

Most of the focus on Obamacare has been on people who are no longer uninsured, or those who had to get new policies, but Kentucky is one of the 13 states in which the Patient Protection and Affordable Care Act helped people in the individual insurance market, according to a study by a fellow of the Brookings Institution.

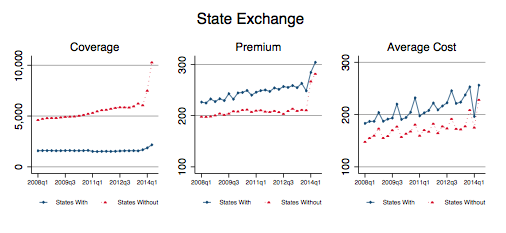

To make comparisons across states, assessing the health law’s impact on coverage, costs and other factors, economics fellow Amanda Kowalski put each state in one of five groups based on how they implemented the law.

Kentucky and seven other states – Colorado, Connecticut, New York, Rhode Island, Vermont and Washington – as well as the District of Columbia, embraced the law completely by setting up their own health-insurance exchanges and expanding the Medicaid program to households with income up to 138 percent of the federal poverty level.

Overall, average premiums grew remarkably in these states, says Kowalski. On average, premiums in Kentucky rose by 16 percent, less than the national average of 24.4 percent, says the report. In the table, states with their own exchanges are represented by blue and states without their own are in red.

However, under Obamacare, premiums don’t tell the whole story, because people earning up to 400 percent of the poverty level are eligible for tax credits that reduce their monthly premium cost. Kentucky’s average cost decreased 19 percent.

This cost decrease, combined with an increase in coverage, suggests that Kentucky’s individual market had been adversely selected. Adverse selection is the tendency for people to avoid buying insurance until they need it, which often drives up insurance premiums. Individual health-insurance coverage in Kentucky increased by 38 percent, with exchange enrollment representing 43 percent of the increase, Kowalski reports.

Kowalski compared states that allowed or did not allow renewal of non-grandfathered insurance plans, in response to complaints that cancellation of their plans contradicted the promise made by advocates of the law that if people “liked their plan they could keep it.” Kentucky and 26 other states grandfathered such plans, and Kowalski concluded that it cost people in their individual markets $220 a year because the people keeping non-grandfathered plans were healthier.

Kentucky was among 41 states that saw increased health-insurance markups, additional amounts charged by insurers beyond the average cost of paying claims. These increases appear to reflect uncertainty about the insurance market; insurance companies had to set premiums without knowing the health status of enrollees and likely protected themselves with markups.

Kowalski’s analysis relies on data from the first half of 2014. “The national experience might evolve over time” and as regulations become more defined within the law itself, the impact of the law will be better understood, she writes.

The study may come as a surprise to critics of the law, who have focused on the many Kentuckians who had to get new health-insurance policies because their old once did not cover the 10 things the law requires.

Some critics continue to say those Kentuckians numbered 280,000, but that number is outdated and incorrect, according to the state Department of Insurance. It’s more like 130,000.

“The 280,000 represented the number of people in the individual and small group markets at the time who potentially could have received a letter saying their health insurance policies were being discontinued because benefits were changing,” department spokesman Ronda Sloan said in an email.

“Those receiving the letters were told the current plan didn’t meet the requirements of the ACA but were offered a new plan that did,” Sloan wrote. “They also were free to shop around either on or off the exchange.”

Of the 280,000 who could have been in jeopardy, “48,302 were in grandfathered plans, so they were not affected,” Sloan wrote. “Another 63,832 were offered transitional relief (President Obama’s request that companies be given the option to extend policies). Most of the remaining group had an option to take early renewal, which would have continued their pre-ACA policies” through at least Dec. 1 of this year. “So, from our perspective, almost everyone in the original 280,000 group had some option to continue existing coverage – and all of them could have moved to an ACA-compliant plan either on or off the exchange.”