Cost of employer-based health insurance grew more slowly after 2010 reform law, but not for single-person plans in Kentucky

Kentucky Health News

The growth in premiums and deductibles for employer-based health insurance has slowed since federal health reform was enacted, but workers probably haven’t noticed because incomes haven’t kept up with the cost of health care, a new study says.

|

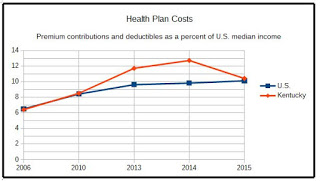

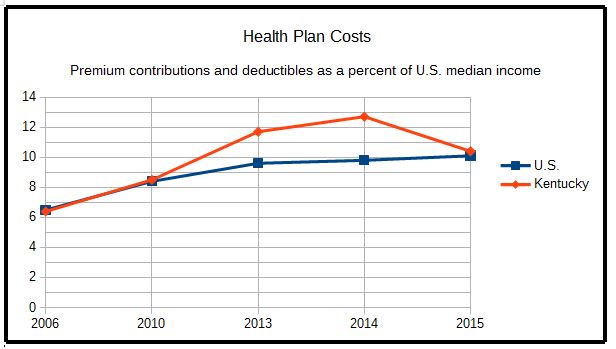

| Kentucky Health News graphic, based on data from Commonwealth Fund report |

Kentucky families covered through employers spent, on average, 10.4 percent of their incomes on health insurance in 2015, slightly above the national average of 10.1 percent, according to an analysis by The Commonwealth Fund, a New York-based research foundation. In 2006, the national average was 6.4 percent, just under Kentucky’s figure a decade earlier, Kentucky’s median family income is less than the national average; in 2015, it was $50,000.

“They’re still facing a bigger burden today even though growth has slowed. . . . because wages have remained largely flat over the last few years,” David Radley, co-author of the report, said during a teleconference.

The study looked at about 154 million Americans under 65 who get health insurance through their employers, using data from the Medical Expenditure Panel Survey and the Current Population Survey.

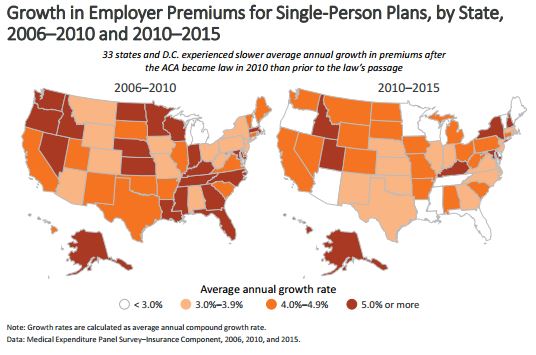

Critics of the law say it has caused higher premiums on employer plans, but Radley said the research shows otherwise. The study found that annual rates of premium growth for single-person plans have slowed in 33 states and the District of Columbia since 2010, compared to earlier years.

But that wasn’t so in Kentucky, where single-person premiums grew at a faster rate between 2010-15 than the rest of the nation: 5 percent, compared to 3.8 percent respectively. That put it in the top eight states for increases.

The report also found that after the passage of the law, employee premium contributions for single-person plans grew more slowly in 31 states, including Kentucky.

Again, Kentucky’s costs were slightly higher. A single-person premium contribution in Kentucky grew 4.7 percent annually after 2010, compared to 6.4 percent before 2010. The national rates were 4.2 percent and 6.7 percent, respectively.

Family plans and deductibles

Employee premium contributions for family plans after passage of the law grew more slowly in 30 states and the District of Columbia, says the report. In Kentucky, this rate was about the same before and after 2010: 5.5 percent and 5.4 percent, respectively. The national rates were 6.5 percent and 4.8 percent, respectively.

The report also found that average deductible growth in single-person plans slowed in Kentucky and 26 other states since 2010, though deductible growth remained high in 22 states and the District of Columbia. In Kentucky, deductible growth was 7.9 percent since 2010, compared to 12.5 percent before 2010. In 2015, Kentuckians paid an average of $1,543 for their deductibles, compared to $659 in 2006. Click here for the Kentucky data.

The report came as the federal government announced increases averaging close to 25 percent for premiums on its insurance exchange, which serves about 10 million people who don’t have employer health coverage. Kentucky’s Cabinet for Health and Family Services has said Kentucky’s exchange plans are increasing by an average of 20 percent. Most people on the exchange will also get an increase in government subsidies, which will ease the impact.

Sara Collins, lead author of the report, said some exchange premium increases likely stem from the fact that the exchange is a much smaller and newer market than employer-based markets and that they are still working to understand their risk pools.

The Patient Protection and Affordable Care Act has several provisions that affect employer-sponsored coverage, such as requiring larger employers to provide health insurance to full-time employees, allowing parents to cover their children up to age 26, and covering preventive services with no cost-sharing. Early predictions were that these requirements would cause many employers to stop offering health insurance, but they haven’t.

“We just have not seen that,” Collins said. “There just hasn’t been large-scale disruption in the employer group market.”

“There has been little change in the number of people with employer-sponsored coverage since the law’s passage in 2010,” Radley added.

The authors attribute the slowdown in health-insurance premiums and deductibles to the slowdown in health-care costs since the implementation of the reform law. Commonwealth Fund President David Blumenthal said, “It would help if employers designed health plans that help their workers afford timely care. But since employer health insurance costs are driven by overall health-care costs, it is also crucial to implement provider payment reform and quality improvement initiatives that keep health-care costs down while improving patient outcomes.”