American Health Care Act would have major impact on Ky. by phasing out Medicaid expansion, changing private insurance

Kentucky Health News

The acronyms may be similar, but the American Health Care Act, Republicans’ replacement for the Patient Protection and Affordable Care Act, would overthrow some core tenets of “Obamacare” and have major impacts on Kentucky.

The ACA and the AHCA are mainly about the individual health-insurance market, where about 7 percent of Americans get coverage, but in Kentucky, the law’s biggest impact is the expansion of the federal-state Medicaid program. About 440,000 Kentuckians get free health care through the expansion, while only 82,000 are enrolled in Obamacare plans subsidized by federal tax credits.

Medicaid expansion would be phased out

Under the ACA, Kentucky and 30 other states expanded Medicaid to people with incomes up to 138 percent of the federal poverty level, now $16,394 for an individual or $33,534 for a family of four.

Under the ACA, this would be phased out over time, and open-ended federal funding for the states would be replaced with block grants based on a certain amount per Medicaid member.

The block grants would grow more slowly than actual costs, so states would have to pay progressively more or reduce expenses, explains Harris Meyer of Modern Healthcare. The bill would increase the percentage of people who are uninsured and raise uncompensated-care costs for hospitals and other health-care providers, Modern Healthcare reports.

Providers and patient-advocacy groups worry that the block-grant structure would drastically cut funding over time, forcing states to cut eligibility, benefits and provider payments. The American Hospital Association, the Catholic Health Association, America’s Essential Hospitals and the Association for Community-Affiliated Plans have all come out in opposition to the bill in its current form, citing concerns about Medicaid, Meyers reports.

Because Medicaid has considerable turnover, as people gain or lose eligibility or choose to enroll or not, the number of people on the expansion would decline over time. The Congressional Budget Office has yet to estimate how many people would lose coverage or how much the bill would cost.

The organizations that oppose the proposed changes to Medicaid have urged lawmakers to wait for the CBO to score the bill’s impact on spending and coverage levels. An early analysis from S&P Global Ratings estimates that four million to six million people now enrolled in Medicaid would lose coverage under the AHCA.

Drug treatment: The bill would eliminate the existing requirement that Medicaid cover basic mental-health and addiction services in states that expanded it, letting the decide whether to include those benefits. This point is of particular concern in states like Kentucky that have been hit hard by the opioid crisis and thus have a greater population in need of addiction treatment services.

“With Kentucky’s current opioid epidemic, we can’t afford to go back to the days when people had no way of getting substance use treatment or behavioral health services,” Dr. Sheila Schuster, board chair of Kentucky Voices for Health, said in a news release on Wednesday. “Over time, Medicaid cuts would give us far fewer options to meet the needs of Kentuckians.”

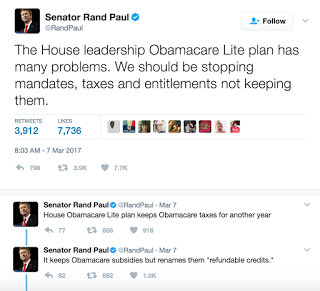

|

| (Image from Twitter; click on it for a larger version) |

Politics: The Republican bill would stop expansion enrollment on Jan. 1, 2020, but conservatives have objected to the delay, and “White House officials are beginning to urge House GOP leadership to include an earlier sunset of the Medicaid expansion,” reports Jeremy Diamond of CNN. But Greg Sargent of The Washington Post writes, “This would mean that the fallout hits right amid the 2018 midterm elections, something that could not only impact the congressional and Senate races, but also the hugely consequential 2018 gubernatorial contests, in which repeal of the Medicaid expansion could create major complications.”

An earlier phase-out of Medicaid expansion would also complicate prospects for the bill in the Senate, where several Republicans want to protect it for their states and GOP leaders can’t afford to lose more than two GOP votes. (Kentucky Sen. Rand Paul is expected to be one; he called the bill “Obamacare Lite” in a tweet on Tuesday, and expressed disapproval of its ACA holdovers.) However, the Senate could take a more moderate stance once it gets the bill and pressure the House to accept that version, NBC reports.

How money would flow: Under the AHCA’s per-capita grant model, states would receive a flat amount of federal dollars for each of five Medicaid beneficiary groups: the elderly, blind and disabled, children, adult expansion beneficiaries and adult non-expansion beneficiaries. States would then decide whom to cover, which benefits to offer and how much to pay providers.

The bill would use fiscal year 2016 as a baseline for each state’s per-capita spending for each of the five beneficiary groups. Those baseline figures would then be trended forward to fiscal year 2019. In 2020, the Department of Health and Human Services would use those figures to compare a state’s spending target with its actual per-capita spending. The target would be calculated using the medical component of the Consumer Price Index, which lags behind actual Medicaid per-capita costs, Meyer notes.

“If a state’s per-capita cost growth exceeded the target, the federal government would take back its excess payments by reducing its contributions in each quarter of the following year,” Meyer reports.

Private insurance would change

One of the biggest changes to private insurance would be how policies are subsidized. The existing program uses advance tax credits to help offset out-of-pocket costs. The tax credits are based on age, income and local insurance prices. (Learn more about how tax credits are calculated here.) The AHCA would offer tax credits based only on age, and with a different structure.

|

|

Graphic from The Economist

|

Lower-income people would get lesser tax credits than they do now, and credits would be available to higher-income people who don’t get them now. Tax credits for small businesses would be eliminated.

Individuals with modified adjusted gross incomes under $75,000, or married couples with MAGI under $150,000, would get the same, fixed amounts for their age groups. People above those thresholds would have their tax credit would be reduced by 10 percent of the income above the threshold.

Tax credits would start at $2,000 a year for people under age 30, increasing in $500 increments per decade in age, up to $4,000 a year for people 60 and older. The credits would be limited to $14,000 per family, FactCheck.org writers explained in USA Today. The new structure would take effect in 2020, with modifications in 2018 and 2019 to give more to younger people and less to older people.

Rural areas are more vulnerable than urban areas to cuts in subsidies because the existing program takes local insurance costs into account and the AHCA does not. Counties in western, southern and southeastern Kentucky are particularly vulnerable to such scenarios. Find out how your county would be affected with this interactive county-by-county map from the nonpartisan Kaiser Family Foundation.

Critics say this structure hurts low-income Americans and benefits the wealthy. “Kentucky has gained more from the Affordable Care Act . . . than any other state, and we have more to lose from its repeal,” Jason Bailey of the liberal-leaning Kentucky Center for Economic Policy said in a news release. “The new House proposal is a plan to give tax breaks to the wealthy paid for by dramatically reducing the number of people with health coverage.”

The AHCA would allows for a wider range in insurance pricing; insurers could charge older individuals up to five times as much as younger people, and states could change that ratio, FactCheck notes. Under current law, the ratio is three-to-one. Thus, young people could see lower premiums while older ones could see higher premiums.

Other provisions: In addition to tax credits, current law offers cost-sharing subsidies to reduce copayments and other out-of-pocket costs for people earning between 100 percent and 250 percent of the federal poverty level. The AHCA would eliminate those subsidies in 2020 but create a Patient and State Stability Fund with $100 billion over nine years that could be used for various purposes, including mitigating out-of-pocket costs.

The AHCA would increase the amount that could be put into tax-exempt health savings accounts, now $3,400 for individuals and $6,750 for families, to $6,550 and $13,100, respectively. The bill also aims to allow people to use HSA money for over-the-counter drugs. Current law allows HSA money to be used for an over-the-counter drug only if the patient first received a prescription for it.

The bill would eliminate the requirement that almost all Americans have health-insurance coverage, but would encourage people to remain insured by letting insurance companies charge a penalty for not having continuous coverage. Insurers could charge 30 percent higher premiums for one year, regardless of health status, to people entering the individual market who had a lapse of coverage of 63 days or more during the previous 12 months.

An early analysis from S&P estimates that 6 million to 10 million fewer people will have health-insurance coverage as a result of the bill. Read a detailed summary of the AHCA here.